9 Biggest Wealth Killers That Keep You Broke In Your 20s and 30s (Must Avoid)

Avoid the most common financial mistakes that destroy wealth. Learn practical strategies for investing, career growth, debt management, and long-term financial success.

The biggest wealth killers aren’t always about what you spend, but more about the life decisions that can drain your bank account without you even realizing it.

Today, we’re discussing wealth killers to avoid in your 20s and 30s, and I promise that there are at least a few ones you’ve never heard of before on any other personal finance platforms.

Wealth Killer #1: Staying In The Wrong City

This is one that nobody really talks about, but geography might be one of the most important financial decisions you can make.

If you grew up somewhere, and there’s just not a lot of industries that align with what you want to do in your career, or perhaps the median salary in your city is dramatically lower than what you could be earning somewhere else, then by staying there, you are costing yourself money.

A city that’s good for your wealth usually has a few parameters.

#1. Good Career Prospects

#2. Quality People

You want to surround yourself with people who are as ambitious as you are with similar goals to yourself.

If you’re able to start in a city with a competitive salary, that’s going to be huge, because if you compound that over time, that’s going to amount to a lot of wealth in your lifetime.

The first salary that you ever get will become the anchor to every salary negotiation that you have in the future.

Pretend you live somewhere in the middle of America, say Kansas City.

Now, if you’re from Kansas City, I’m not trying to throw shade at you. I’m just trying to illustrate that the median household income in Kansas City is $69,000 a year.

If you were to move to Austin, Seattle, Boston, or San Francisco, the median jumps quite a bit.

So, Austin has a median household income of $90,000 per year, and San Francisco is over $135K, just as examples.

Even if your cost of living goes up somewhat, if you can keep it reasonable, you’re basically arbitrage the geographic difference in salary every year.

A few years ago, I visited a gold factory in Switzerland out of all places, and what was really fascinating was that it was really close to the Italian border.

What was fascinating was that a lot of people who worked in the factory were from Italy itself, and that was just across the border.

They wanted to work in Switzerland because the wages in Switzerland were just that much higher.

So, what you had were Italian workers going into a Swiss gold factory, and then they could take that wage and go right across the border back to their hometown in Italy, where the cost of living was much cheaper.

That’s an extreme example, but it’s the same principle of geographic arbitrage.

The other thing that’s underrated here is your network. So, I really do feel like you can make a lot of money based on the quality of your network and the people that you meet.

The opportunities we get exposed to and the introductions we receive, all of that is going to be highly dependent on where you actually live.

You can always move back to your hometown once you’re established, but building your career in a low-opportunity city by default is a huge wealth killer that many people don’t even talk about or think about, and it happens a lot in your 20s and your 30s.

Wealth Killer #2: Overfunding Your Emergency Reserves

A lot of you guys reading now might fall into this trap because you want to be good with your money.

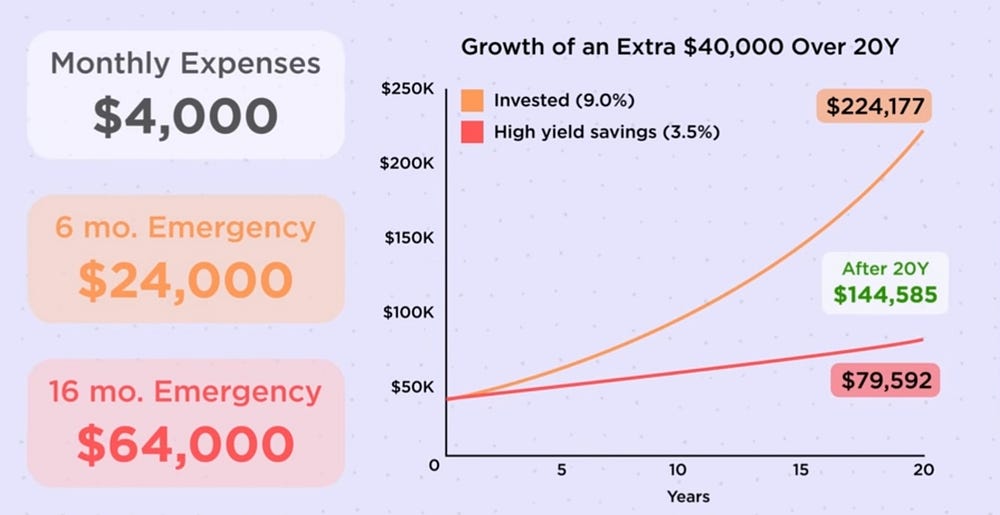

In a typical emergency fund, you want to have between three and six months of living expenses saved up just for emergencies.

That’s just so that in case you lose your job, you still have some sort of funds to rely on so that you can pay your bills, live your life, find a new job, etc.

But, I personally know people who keep $80,000, $100,000, $167,000 in a high-yield savings account just because

- It makes them feel better.

- They like the idea of having a really big buffer between them and a catastrophic emergency.

But when you have 16 to 24 months of expenses parked in cash or even more, that excess money is costing you money in terms of opportunity cost.

Say your monthly expenses are $4,000 a month, a 6-month emergency fund would be $24,000, and a 16-month one would be $64,000.

The difference there is $40K, and that extra $40K sitting in a high-yield savings account at 3.5% instead of being invested in the market at roughly 8 to 9% could cost you about $145,000 over 20 years.

The point here is just to be intentional about how much you actually need. So, anything beyond 6 months that you’re holding in cash just in case could just be a symptom of having a scarcity mindset.

I definitely get it if you want to be safe with your money, but just make sure you’re not being too safe.

Wealth Killer #3: Divorce

I think divorce really emphasizes the fact that finding a good partner is one of the most important decisions of your life.

The US has the sixth-highest divorce rate in the world, with 40 to 50% of married couples filing for divorce.

And the stat that’s even crazier is that the second and third marriages have a divorce rate of 60% and 73%, respectively.

That means if you get divorced the first time, the likelihood that you get divorced a second or a third time is much, much higher.

And you think with all these divorces that people would get prenups, but that’s actually not the case either, because only 15% of married couples report signing a prenup.

Here are the top reasons for divorce.

They include lack of commitment at 75%, infidelity at 60%, too much conflict at 58%, and, as you can see here, financial problems, getting married too young sit between 37% and 45%.

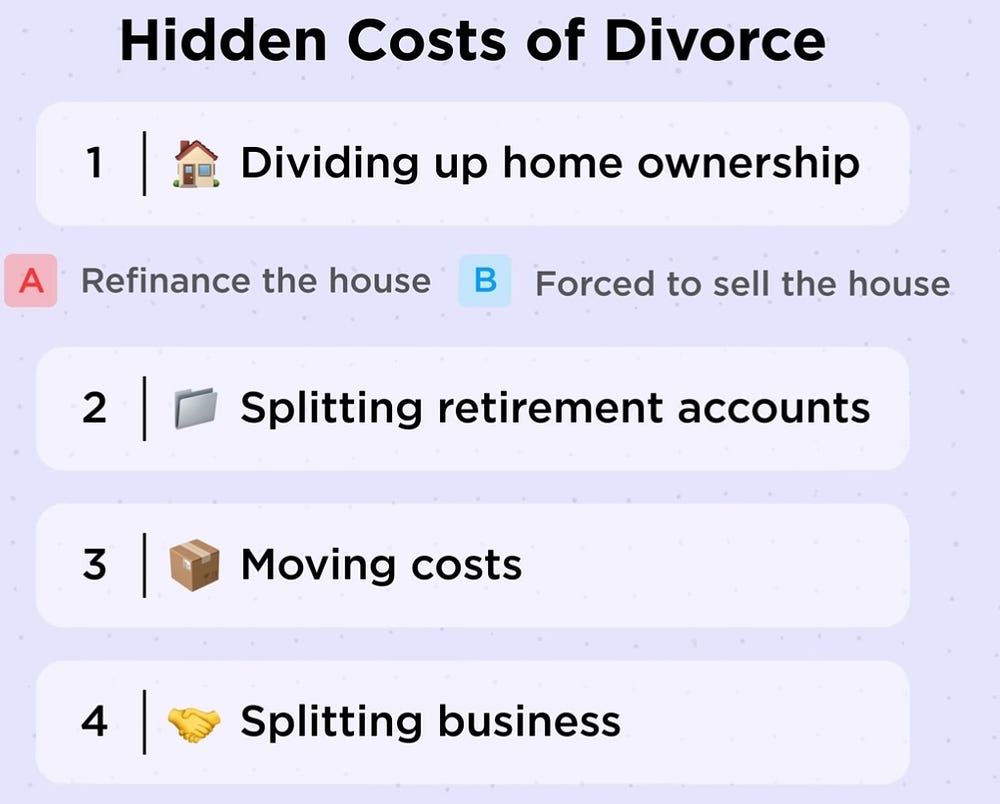

So, why is this such a wealth killer? Well, obviously, the cost of the divorce itself is quite expensive. It can easily run you over $20,000.

But the hidden costs of divorce are actually what add up to a lot more, in my opinion.

So, let’s say, for example, you own a home theater. If you were to split up, that often means you have to refinance the house at whatever the current interest rate is, which, as we’ve seen recently, has not been good.

The other option is that you just sell the house, and perhaps you’re forced to sell it during a bad market, and you could lose a lot of money that way.

Then, if you have retirement accounts, you have to split those, and those require a specific court order, and you might even face taxes and penalties for early withdrawals.

Don’t forget about moving costs as well, and if you want to split up furniture or physical assets, that can take a toll.

And if either one of you owns a business that was started during the marriage, that can get very, very complicated, too.

If you add up all the hidden costs plus the normal cost of divorce via legal fees, it could run you up to $50,000 to $100,000 and even sometimes more if you have a lot to lose.

The bottom line is that who you marry is, unfortunately and fortunately, one of the most consequential financial decisions in your life.

You want to get it right, but if you get it wrong, you could undo a lot of wealth building that you made in your early years.

Wealth Killer #4: Trying To Look Rich

There’s a phrase in the financial world that’s been around for decades, and it’s called keeping up with the Joneses.

The reason why this phrase has stuck around is that it describes one of the most fundamentally destructive behaviors that we all fall for.

And that behavior is trying to keep up with your friends.

When you’re going through life, it’s natural to want to measure your own financial success against what other people appear to have, like your neighbors, your friends, or just people on Instagram.

But if you do that, that’s when you’ve lost.

A lot of what you see is what people want you to see, either in person or online, and that’s usually controlled and calculated as long as they’re aware of their image.

All you see is a highlight reel, but what’s really going on behind the scenes of someone’s life is something that you don’t really have access to.

The new car might be leased, the designer clothes could be borrowed, and the apartment that looks super bougie and chic on Instagram might be taking up 60% of that person’s take-home pay.

A $30K millionaire is an individual who makes $30K a year, but acts like they make millions, essentially doing everything in their power to flex on other people.

According to Urban Dictionary, quote, “Someone who goes to the club and pays to get the VIP table, but then they can’t buy any drinks because they spent all the money on the table.” What a $30K millionaire.

The lesson here is that the people who look like they have money, they don’t have any money, and the people who don’t look rich are usually the ones who are mega-rich.

I personally think that if you’ve been building wealth for a long time by staying focused, you stay in your lane, and you live below your means, you’re going to get wealthier than someone who is trying to constantly compare themselves to others.

Wealth Killer #5: Optimizing For Salary Instead Of Equity

This one is super relevant if you’re working for a startup or a company that offers stock-based compensation, but it’s also important enough to talk about in general, as well.

A lot of jobs these days, especially if you’re working for a public company, a startup, or perhaps a company on its way to IPO, are going to offer you equity as part of your total compensation.

During the negotiation process, you usually have a little bit of flexibility here. You can either opt for a high base salary and less equity, or you can have more equity and less of a base salary.

A lot of people opt to take the higher base salary because they want that cash in hand, which gives them more cash flow and allows them to perhaps rent a nicer apartment, or perhaps inflate their lifestyle a little bit.

But here’s the thing: a single good equity outcome can actually outperform an entire decade of salary or more.

Of course, this is very dependent on where you work. I definitely understand that not everyone is going to work for a company like SpaceX, Google, or Nvidia.

But, in most cases, if you’re offered some sort of equity at a mid-size to large company, and you believe in that company, it’s my personal opinion that I think you should be taking more equity than cash, because at least there’s some upside with equity.

Now, of course, this all comes with a huge disclaimer, which is that you have to do your due diligence on the company itself, and if it’s actually going anywhere.

If your friend has a brand new startup run out of his garage, you might want to think twice about the risk that comes with that role, and if you want cash or equity instead.

When it comes to figuring out what your potential equity is worth, I would do two things here.

#1. I would figure out what my equity is worth as a percentage of the company.

If a company offers you 10,000 shares, that’s not very meaningful unless you know how many shares are actually outstanding.

But, if you do the math and figure out how much your shares are actually worth in terms of equity, you can get the total share count from your HR department or legal department. Hopefully, you can then figure out what percentage of the company you own.

#2. Which is to figure out what your company is worth currently or what it will be worth in the future if it ever has a liquidation event or an IPO.

If you own 0.1% of the company and your company ends up IPOing for say a hundred million dollars, then your equity is worth 0.1% of that, or $100k.

If you need more practice with that sort of thing, you might want to watch the TV show Shark Tank, because they actually often walk through evaluation numbers quite often.

And I think if you watch that show enough, you start to get it through repetition.

Wealth Killer #6: Staying on the Sidelines (Investing)

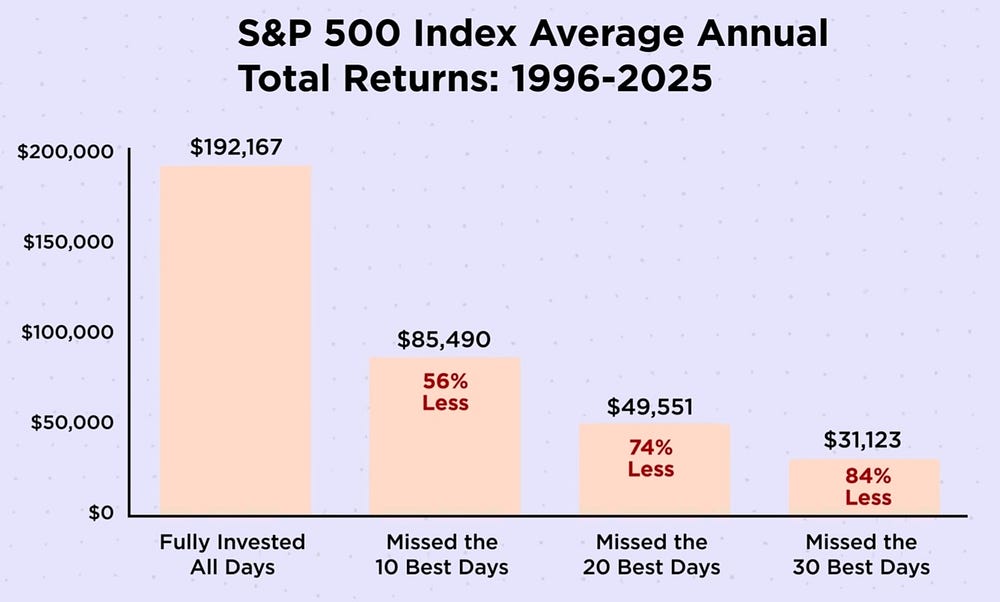

When we wait around to invest, that’s the most guaranteed way of not making any money.

Here’s the hypothetical growth of $10,000 invested in the S&P 500 index from 1996 to 2025. You can see that if you’re fully invested all the days, your balance would be over $192,000, but if you miss just the 10 best days in that time period, your gains would be 56% less. And the chart actually gets way worse.

So, if you miss 20 of the best days, your gains are 74% less, and if you miss 30 of the best days, you’re looking at 84% less gains.

Your portfolio growth is influenced heavily by being invested in the best-performing days of the market, so you really can’t afford to lose any of those best days.

Unless you are retiring soon and need to preserve your short-term wealth, it is often better to simply try to stay in the market as long as you can rather than trying to time it for dips.

I think so often many people just stay in cash, or they just want to wait till the market cools off a bit.

I have a lot of friends who do this, but I think that if they aren’t at least earning the same rate as inflation, then their purchasing power is getting eroded by inflation itself.

If you don’t want to invest for whatever reason, at a minimum, you should keep cash in a high-yield savings account while the interest rates are decent.

Wealth Killer #7: Sunk Cost Loyalty

This wealth killer is about the tendency to stay in a job longer than you should, just because it’s comfortable, familiar, or you just like all the co-workers that you work with.

But, being loyal can actually be a double-edged sword because if you stay at a company too long and they’re only giving you, let’s say, a 3% to 5% raise every single year, you’re just not going to make that much money, especially if you’re coming from a place where you started with a low base salary.

Let’s say you got a job out of college and you worked at, say, the Marriott Hotel Group, and you started with a salary of $60,000 per year.

Corvette, every 2 years, they will give you a cash raise of 3%. You work there for 10 years, and at the end of those 10 years, your salary is $70,000 a year.

And that’s not really a big pay bump, especially if you’ve been working for some place for 10 years.

For me personally, I wasn’t the type of person to go into my boss’s office and demand a raise.

I was personally taught that I was just lucky enough to have a job, especially because I graduated around the financial recession of 2008.

And I’m sure many of you probably feel this way, especially because of all the layoffs that have been happening in America right now.

You probably don’t want to rock the boat with your employer. But the reality is that companies are just not running around trying to give you raises left and right.

They are going to give you exactly what they have to and not a penny more.

So, if you don’t ask for a raise or stick up for yourself, you’re just volunteering to give up your potential value.

One other strategy you could perhaps try to get out of this wealth killer is if you switch jobs every couple of years, especially if you’re at the beginning of your career.

If you’re able to switch jobs, you can reset the base salary when you do your negotiations, and usually this will result in a pay bump.

According to a study from LendingTree, workers who switched jobs saw their average earnings jump over 11% and, in some cases, even upwards of over 30%.

The idea here is that you want to be switching every 1 to 2 years so that you either go laterally in job title and increase your pay, or you go laterally in terms of pay increase but increase your job title.

Either way, as long as you’re consistently doing this and increasing your job title or your pay, by the time you are in your mid to late 30s, your salary has been bumped up multiple times, and your wealth can continue its own growth.

Wealth Killer #8: High-Interest-Rate Debt

Now, there are some cases in which borrowing money is actually okay, and I believe that not all debt is bad.

I would argue that getting a mortgage to buy a home or getting a student loan for a degree that pays off later, these are calculated uses of leverage.

In these cases, you’re borrowing money to acquire something that should appreciate or produce income for you in the future, so in those cases, I think that is pretty good debt.

The problem in America is high-interest-rate debt, especially credit card debt or any debt that has an interest rate of over 10%.

The average APR for credit cards is 22.11% as of 2026, and that means on a $10,000 credit card balance, you will pay roughly $185 in interest every month as part of your payment.

And if you have to pay these interest payments, then obviously you can’t use that money for anything else.

Trying to build wealth for the future is going to be really tough because a lot of your money is going to go straight to interest.

So, if you’re in your 20s or 30s, I think one of the best financial decisions that you can make is to never carry high-interest-rate debt from month to month, and this is just going to save you a lot of headaches in your life.

Wealth Killer #9: Buying Too Much of a Car

You know that a car is a silent wealth killer because not only are you paying car payments, but you have to pay hidden costs as well.

Insurance, maintenance, depreciation, and gas, those all add up over time. The average price of a new car in 2026 was over $51,000, which translates to a new car payment of over $750 a month, or that’s about $9,000 a year.

Then, if you add in insurance and depreciation, the true cost of owning a car is easily over a thousand bucks a month.

At an 8% average return, if you invested those payments instead, in 10 years, it would be worth over $213,000.

But that argument isn’t the best one because it also assumes that you would give up driving a car altogether.

So, instead, may I suggest that you drive a reliable used car instead, because the average used car payment is $537 a month, which is $213 less per month than the new car.

You’re still going to have the same commute, and your life pretty much stays the same, but $213 a month invested over 10 years is worth over $45,000.

That’s $45K for doing nothing different except choosing a used car over a new one.

Our society attributes status and prestige to having a ride, and so much of our identity is wrapped up in what kind of car we drive.

So, if that’s the case and that’s you, and you still want to save some money, I still think it makes a lot of sense to buy a car that has around 30,000 miles or is around 3 years old.

You’re still getting a great deal on the car, you’re driving a car that’s not too used, so it still seems brand new, and you’re going to save money on your total cost of ownership.

Thanks For Reading 🙂